A while back, I read a sensational paper who was trying to scare us 🙀(classic, I know). He wrote that he was amazed of the cost of paying a 70 years annuity to an exec who left early with reprimand! Wow, given the cost of an annuity, how titanic would a 70 years annuity be worth? Well the journalist did not explore the exact cost 🙉, but continued to ramble on the excessiveness of this golden parachute. For an actuary, I think that the journalist left a golden nugget there. Sadly, a 70 years annuity is well not that of a high price tag versus a classic 30 years annuity.

One reason to look at this subject is that one of the fear 🙀of the FIRE, Financially Independant Retire Early, community is the fear of longevity. How much more a 30 years annuity is compared to that of an 70 years annuity...

First, why would you want a 70 years annuity if you are not an executive? That would be like having an annuity for yourself and your children. The game “The Talos Principle” illuminated my though on the subject. The little robot🤖you play is the millionth generation of a serie of “IA”. Each previous generation died trying to escape various trap and puzzle. Each generation slowly learning to get better. At the game end, you prove that you are finally a robot🤖worth waking up. I reflected that we are also a generational species. We build on the shoulder of giants. From a financial perspective, both my grand father and father were not rich. Quite middle income. Although that is true, it is also true that if the earlier would have put 10$ in the S&P500 in 1900 (roughly 250$ in current day), I would be a millionaire 💰. (source: OfficialData.org). Why didn’t my father given me 10,000$ when I was born? I would have been already a millionaire 💰.

Why would we want the next generation to start from nothing? The trill of the hardship? I never lived near the rich. Never seen the silver spoon effect. However, I have seen my fair share of adult with no aspiration. None of them were rich or started rich. Why really wonder how many wealthy do nothing of their lives vs poor one. It is great to have dreams and grits but I fail to see how it is related to the lack of money. Having infinite money means that you can procure what ever you want. Having a dream to do something do not require any money. Having money do not preclude someone to dream. Between having debt up to my eye ball or having a 6 figure net worth, I would select to be rich💸. Thus it make sense to try to attained a generational annuity.

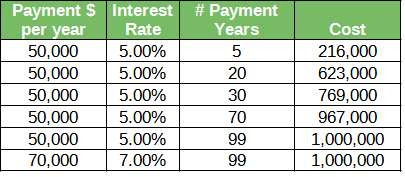

From my actuarial background, I have learn the formula for calculating the worth an annuity. At 5% interest rate, a 50k yearly payment for 5 years is worth about 215k. It make sense. If you kept 250k aside, it would provide for exactly 5 year worth of 50k. At 5% return, you get a small discount of 35k. Interestingly, if you wanted a 20 year 50k fixed annuity at 5%, it would not cost 4x. It cost 620k. The trick here is that 5% interest on 1 million dollar is 50k. 1 million💰offer an eternal yearly payment of 50k. Compared to a 30 years annuity (like would you probably elect at 65 to provide a lifetime ending at age 95) cost 770k so for 30% more, instead of having a finite pension, you get an infinite one.

IQPF, which relies on historical data, expert opinion, RPC and RRQ, provide that roughly the expected rate of return in the future should be about 7% if you invest 100% in equity. Thus 1 million💰would provide either 70k annuity per year or 50k + 2% increase per year (to offset inflation).